CIBIL Score is a three-digit number that ranges between 300 and 900 and indicates your creditworthiness. Scores closer to 900 represent better creditworthiness and vice versa. Banks typically consider a credit score of 700 or higher when you apply for personal loans, mortgages, credit cards, overdraft facilities, etc. It is calculated based on your credit behavior, including credit utilisation, repayment history, and credit duration.

Let’s examine the step-by-step procedure regarding CIBIL score check for free via the Doloans website:

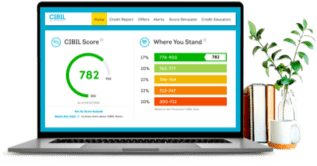

Within 300–900, lenders typically group scores into five levels:

| Aspect | CIBIL Score | Credit Score |

|---|---|---|

| Definition | This is a numerical representation of your credit history provided by TransUnion CIBIL, a widely used credit bureau company in India. | Any credit bureau in India, including CIBIL, Experian, CRIF High Mark, and Equifax, can numerically represent your credit history. |

| Usage | Lenders use your CIBIL Score to assess creditworthiness when you submit a credit application for personal loans, car loans, mortgages, credit cards, etc. | Lenders use your Credit Score to assess your creditworthiness when you submit a loan/credit application. Each bureau’s score would be considered equally and taken as an average. |

| Range | 300 to 900, with scores above 750 considered excellent and above 700 considered good. | Typically 300 to 900, where a higher score indicates better creditworthiness. |

| Access | An applicant may check their CIBIL score for free via the official website of Doloans. | Credit scores can be checked via the official websites of India’s four credit bureau companies. |

Your track record of paying credit card bills and loan EMIs. Timely payments help; missed payments harm. This can influence ~30% to 35% of your score.

How much credit you use vs. your total available limit. Lower utilisation generally helps. This can influence ~25% to 30%.

A mix of secured and unsecured credit plus longer credit history can help. This can influence ~25%.

Enquiries, outstanding loan amount, and other minor signals. This can influence ~10% to 20%.

A CIBIL Report (Credit Information Report or CIR) is prepared by TransUnion CIBIL and provides an overview of your creditworthiness. It includes personal details, employment data, and your loan/credit card history (accounts, balances, payment history). This information is summarised into the CIBIL Score (300 to 900). Lenders use it to assess risk and determine approval, interest rates, and terms.

Hard inquiries happen when a lender checks your report for a loan/credit card application, and they can slightly reduce your score. Many hard inquiries in a short period can indicate credit hunger. Soft inquiries (like checking your own score) do not affect your score.

| CIBIL Score Range | Creditworthiness | Approval Chances |

|---|---|---|

| 750 – 900 | Excellent | Very High |

| 700 – 749 | Good | High |

| 650 – 699 | Fair | Moderate |

| 600 – 649 | Subnormal | Low |

| Below 600 | Poor | Very Low |

Our consent withdrawal policy states that you can revoke the usage of the information you have provided to Doloans during the CIBIL score check process. Upon withdrawal, your information shall be discarded from our database, unless retention is legally required for compliance, fraud investigations, or regulatory requirements. If your application has been forwarded to a partnered institution, that partner may continue processing information as permitted by law until the credit facility is closed.